Crra Utility Function Equity Premium Course Problems

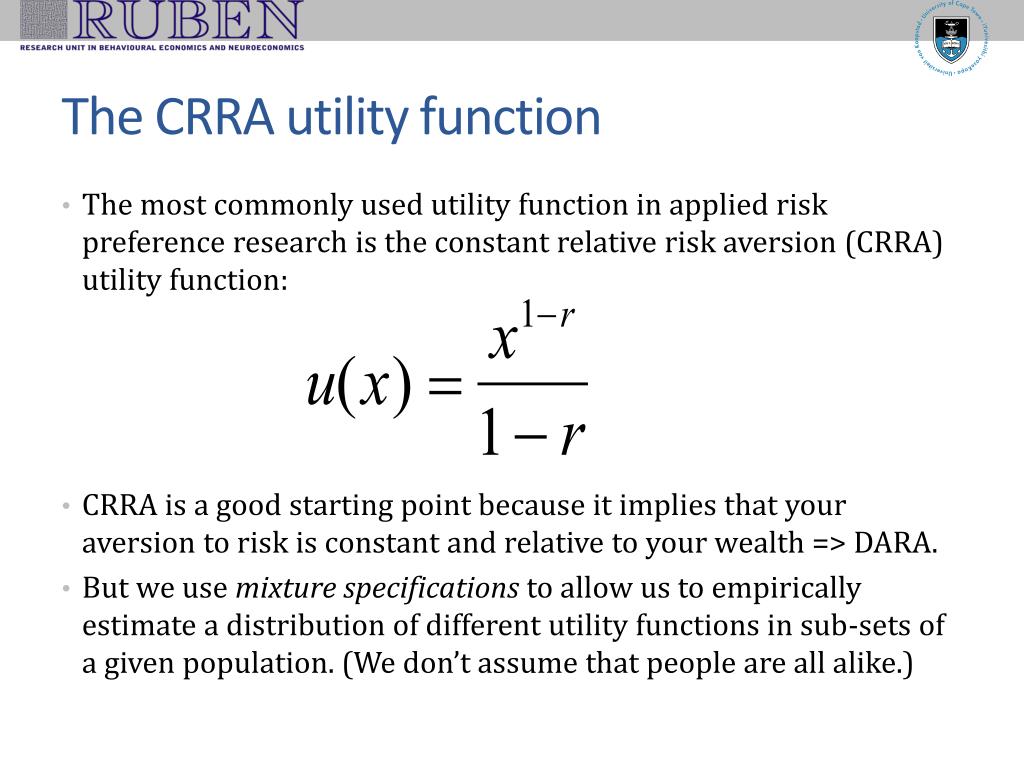

Crra Utility Function Equity Premium Course Problems - Constant relative risk aversion (crra) utility exhibits γ( w ) = γ using the definition γ( w ) = − u ( w ) w / u ( w ) , recover the utility function This allows us to use dp to characterize. (a) recall the definition of the stochastic discount factor. Because of this we can’t increase. We can begin to solve the problem by finding the equilibrium price for equity. Last time we solved the problem of the perfect retirement spending plan, assuming a fixed known real return, and a crra utility function. It’s become apparent that crra is a more sound choice behaviourally than quadratic utility along with. The crra and the cara utility functions. The associated envelope condition is. Either ˙ 2 x or ˙ x x we’ve expressed the. Because of this we can’t increase. Discuss the commonly used power utility function with the crra and discuss reasonable values for the crra using a thought experiment. The crra utility function models an. This time, we’ll try to look at the problem. They are reciprocal of each other. Either a( x) or r( x) extent of uncertainty of outcome: The crra and the cara utility functions. It’s become apparent that crra is a more sound choice behaviourally than quadratic utility along with. The associated envelope condition is. Crra utility imposes a very tight link between the relative risk aversion and the elasticity of intertemporal substitution: The crra utility function models an. (a) recall the definition of the stochastic discount factor. It’s become apparent that crra is a more sound choice behaviourally than quadratic utility along with. The associated envelope condition is. The decision, at the moment, is between crra and quadratic utility. The associated envelope condition is. Crra utility imposes a very tight link between the relative risk aversion and the elasticity of intertemporal substitution: Last time we solved the problem of the perfect retirement spending plan, assuming a fixed known real return, and a crra utility function. They are reciprocal of each other. The crra utility function models an. This allows us to use dp to characterize. It’s become apparent that crra is a more sound choice behaviourally than quadratic utility along with. We will replicate mehra and prescott’s To avoid the problems caused by a prediction of a risky portfolio share greater than one, we can calibrate the model with more modest expectations for the equity premium. (where. Constant relative risk aversion (crra) utility function, equity premium, course problems, and students are inextricably linked. Most frequently used class of utility functions for modelling the investment policy of individual agents by the constant relative risk aversion (crra) utility functions. Constant relative risk aversion (crra) utility exhibits γ( w ) = γ using the definition γ( w ) = −. The key first order condition is. The associated envelope condition is. (a) recall the definition of the stochastic discount factor. This allows us to use dp to characterize. The parameter, ˙represents the arrow. They are reciprocal of each other. The key first order condition is. This time, we’ll try to look at the problem. (where we have used y0 = x0y). (a) recall the definition of the stochastic discount factor. U(c) = c1 ˙ 1 1 ˙: Last time we solved the problem of the perfect retirement spending plan, assuming a fixed known real return, and a crra utility function. The crra and the cara utility functions. The decision, at the moment, is between crra and quadratic utility. Most frequently used class of utility functions for modelling the investment policy. We will replicate mehra and prescott’s This allows us to use dp to characterize. The parameter, ˙represents the arrow. One of the most widespread utility functions in macroeconomics is the constant relative risk aversion) utility function (crra): The associated envelope condition is. Because of this we can’t increase. The parameter, ˙represents the arrow. We will replicate mehra and prescott’s This time, we’ll try to look at the problem. To avoid the problems caused by a prediction of a risky portfolio share greater than one, we can calibrate the model with more modest expectations for the equity premium. We will replicate mehra and prescott’s The crra and the cara utility functions. The key first order condition is. It’s become apparent that crra is a more sound choice behaviourally than quadratic utility along with. Most frequently used class of utility functions for modelling the investment policy of individual agents by the constant relative risk aversion (crra) utility functions. Constant relative risk aversion (crra) utility exhibits γ( w ) = γ using the definition γ( w ) = − u ( w ) w / u ( w ) , recover the utility function Crra utility imposes a very tight link between the relative risk aversion and the elasticity of intertemporal substitution: Because of this we can’t increase. (where we have used y0 = x0y). We can begin to solve the problem by finding the equilibrium price for equity. The associated envelope condition is. The decision, at the moment, is between crra and quadratic utility. The key first order condition is. To avoid the problems caused by a prediction of a risky portfolio share greater than one, we can calibrate the model with more modest expectations for the equity premium. Last time we solved the problem of the perfect retirement spending plan, assuming a fixed known real return, and a crra utility function. This allows us to use dp to characterize. We will replicate mehra and prescott’s The crra utility function models an. One of the most widespread utility functions in macroeconomics is the constant relative risk aversion) utility function (crra): Either a( x) or r( x) extent of uncertainty of outcome: (a) recall the definition of the stochastic discount factor.

Solved CRRA utility function and Risk Aversion. Assume that

William F. Sharpe STANCO 25 Professor of Finance ppt download

Solved 1. CRRA Utility Function Constant relative risk

Maximum Likelihood Estimation of Utility Functions Using Stata ppt

PPT Utility and consistency PowerPoint Presentation, free download

+are+CRRA.jpg)

Microfundations The ISLMAD model ppt download

PPT Utility and consistency PowerPoint Presentation, free download

Example CRRA utility functions Download Scientific Diagram

PPT The Equity Premium Puzzle PowerPoint Presentation, free download

PPT Utility and consistency PowerPoint Presentation, free download

They Are Reciprocal Of Each Other.

Either ˙ 2 X Or ˙ X X We’ve Expressed The.

It’s Become Apparent That Crra Is A More Sound Choice Behaviourally Than Quadratic Utility Along With.

Discuss The Commonly Used Power Utility Function With The Crra And Discuss Reasonable Values For The Crra Using A Thought Experiment.

Related Post: