Oklahoma Form 561

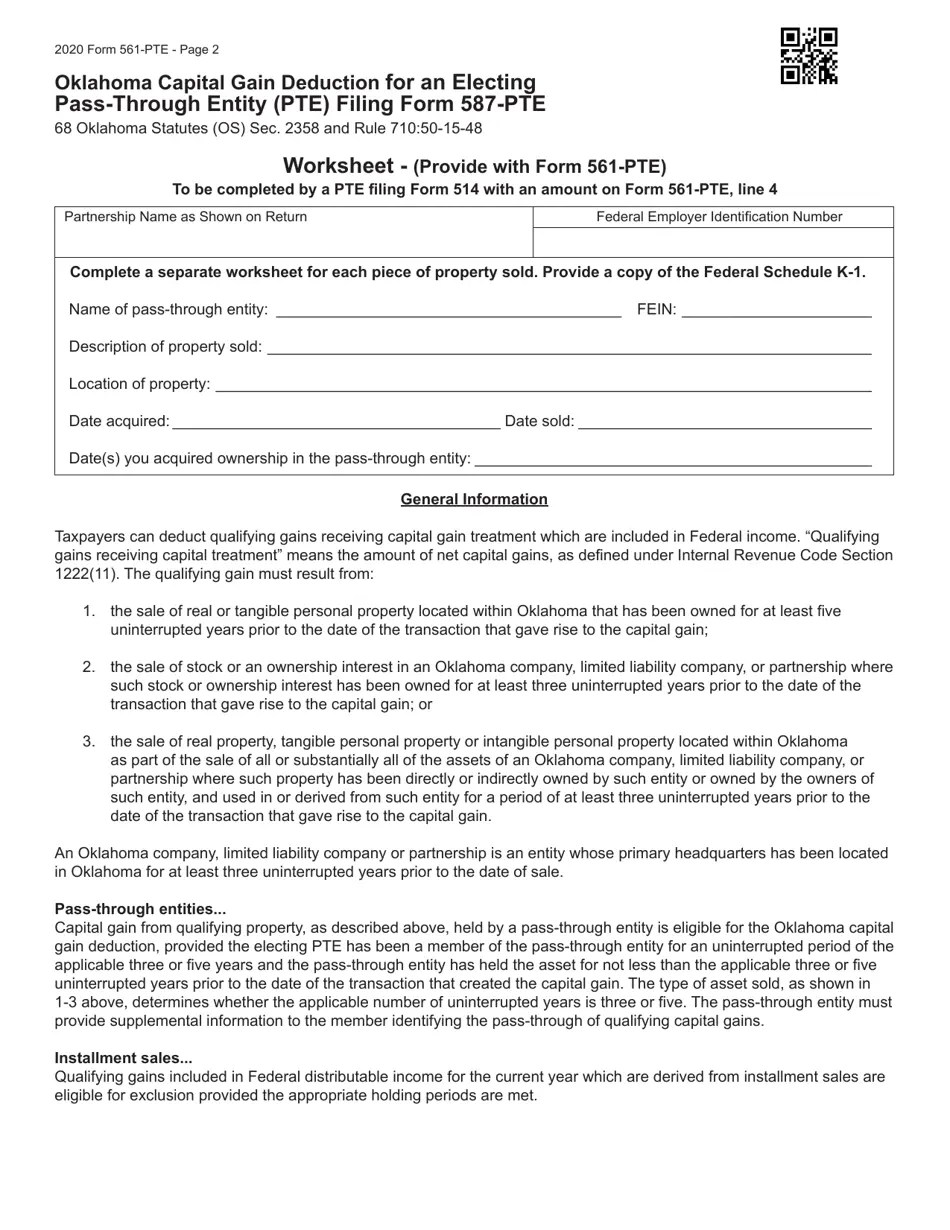

Oklahoma Form 561 - The sale of real or tangible. Individual taxpayers can deduct qualifying gains receiving capital gain treatment that are included in federal adjusted gross income. Do not include gains and losses reported on form 561 lines 2 through 5. The oklahoma capital gain deduction may not exceed the oklahoma net capital gain included in federal adjusted gross income. Qualifying oklahoma net capital gain or (loss) from partnerships, s corporations, estates or trusts reported on federal schedule d, line 12. Qualifying gains receiving capital treatment means the. The sale of real or tangible personal property located within oklahoma that has been owned for at least five uninterrupted years prior to the date of the transaction that gave rise to the capital gain; The ok form 561 is to claim a deduction from ok income of capital gains derived from the sale of property held for two or five years specifically: Qualifying gains included in an individual taxpayer’s federal adjusted. Qualifying gains included in federal distributable income for the. The sale of real or tangible personal property located within oklahoma that has been owned for at least five uninterrupted years prior to the date of the transaction that gave rise to the capital gain; Qualifying gains included in federal distributable income for the. The sale of real or tangible. Do not include gains and losses reported on form 561 lines 2 through 5. To determine the oklahoma net capital gain,. If federal form 6252 was used to report the installment method for gain on the sale of eligible property on the. Qualifying oklahoma net capital gain or (loss) from partnerships, s corporations, estates or trusts reported on federal schedule d, line 12. List qualifying oklahoma capital gains and losses from federal form(s) 8949, part ii or from federal schedule d, line 8a. The ok form 561 is to claim a deduction from ok income of capital gains derived from the sale of property held for two or five years specifically: Qualifying gains included in an individual taxpayer’s federal adjusted. The ok form 561 is to claim a deduction from ok income of capital gains derived from the sale of property held for two or five years specifically: The sale of real or tangible. To determine the oklahoma net capital gain,. The sale of real or tangible personal property located within oklahoma that has been owned for at least five. The sale of real or tangible personal property located within oklahoma that has been owned for at least five uninterrupted years prior to the date of the transaction that gave rise to the capital gain; Qualifying gains included in an individual taxpayer’s federal adjusted. Do not include gains and losses reported on form 561 lines 2 through 5. Qualifying oklahoma. The sale of real or tangible personal property located within oklahoma that has been owned for at least five uninterrupted years prior to the date of the transaction that gave rise to the capital gain; Qualifying oklahoma net capital gain or (loss) from partnerships, s corporations, estates or trusts reported on federal schedule d, line 12. Qualifying gains receiving capital. To determine the oklahoma net capital gain,. The sale of real or tangible personal property located within oklahoma that has been owned for at least five uninterrupted years prior to the date of the transaction that gave rise to the capital gain; Learn how to accurately report stock capital gains and losses in oklahoma with form 561, including filing criteria. Qualifying oklahoma net capital gain or (loss) from partnerships, s corporations, estates or trusts reported on federal schedule d, line 12. List qualifying oklahoma capital gains and losses from federal form(s) 8949, part ii or from federal schedule d, line 8a. If federal form 6252 was used to report the installment method for gain on the sale of eligible property. To determine the oklahoma net capital gain,. The sale of real or tangible. Do not include gains and losses reported on form 561 lines 2 through 5. Qualifying gains included in federal distributable income for the. Qualifying gains receiving capital treatment means the. To determine the oklahoma net capital gain,. Qualifying gains included in federal distributable income for the. List qualifying oklahoma capital gains and losses from federal form(s) 8949, part ii or from federal schedule d, line 8a. The oklahoma capital gain deduction may not exceed the oklahoma net capital gain included in federal adjusted gross income. Individual taxpayers can deduct qualifying. The ok form 561 is to claim a deduction from ok income of capital gains derived from the sale of property held for two or five years specifically: If federal form 6252 was used to report the installment method for gain on the sale of eligible property on the. Qualifying oklahoma net capital gain or (loss) from partnerships, s corporations,. Do not include gains and losses reported on form 561 lines 2 through 5. List qualifying oklahoma capital gains and losses from federal form(s) 8949, part ii or from federal schedule d, line 8a. Qualifying gains included in an individual taxpayer’s federal adjusted. To determine the oklahoma net capital gain,. Individual taxpayers can deduct qualifying gains receiving capital gain treatment. Qualifying gains receiving capital treatment means the. List qualifying oklahoma capital gains and losses from federal form(s) 8949, part ii or from federal schedule d, line 8a. Do not include gains and losses reported on form 561 lines 2 through 5. Qualifying gains included in an individual taxpayer’s federal adjusted. Qualifying oklahoma net capital gain or (loss) from partnerships, s. Qualifying oklahoma net capital gain or (loss) from partnerships, s corporations, estates or trusts reported on federal schedule d, line 12. Learn how to accurately report stock capital gains and losses in oklahoma with form 561, including filing criteria and necessary documentation. The ok form 561 is to claim a deduction from ok income of capital gains derived from the sale of property held for two or five years specifically: The sale of real or tangible. To determine the oklahoma net capital gain,. Qualifying gains included in an individual taxpayer’s federal adjusted. Do not include gains and losses reported on form 561 lines 2 through 5. The sale of real or tangible personal property located within oklahoma that has been owned for at least five uninterrupted years prior to the date of the transaction that gave rise to the capital gain; Individual taxpayers can deduct qualifying gains receiving capital gain treatment that are included in federal adjusted gross income. Qualifying gains receiving capital treatment means the. If federal form 6252 was used to report the installment method for gain on the sale of eligible property on the.

Form 561PTE Download Fillable PDF or Fill Online Oklahoma Capital Gain

Form 586 Download Fillable PDF or Fill Online PassThrough Entity

Oklahoma Form 561 pass through entity

Fillable Form 561 Oklahoma Capital Gain Deduction For Residents

Fillable Form 561 Oklahoma Capital Gain Deduction For Residents

Form 561 NrF Capital Gain Deduction For Trusts And Estates 2009

Fillable Form 561 C Oklahoma Capital Gain Deduction For Corporations

Oklahoma Form 561Nr ≡ Fill Out Printable PDF Forms Online

Fillable Form 561s Oklahoma Capital Gain Deduction 2016 printable

Oklahoma Form 561 pass through entity

List Qualifying Oklahoma Capital Gains And Losses From Federal Form(S) 8949, Part Ii Or From Federal Schedule D, Line 8A.

The Oklahoma Capital Gain Deduction May Not Exceed The Oklahoma Net Capital Gain Included In Federal Adjusted Gross Income.

Qualifying Gains Included In Federal Distributable Income For The.

Related Post: